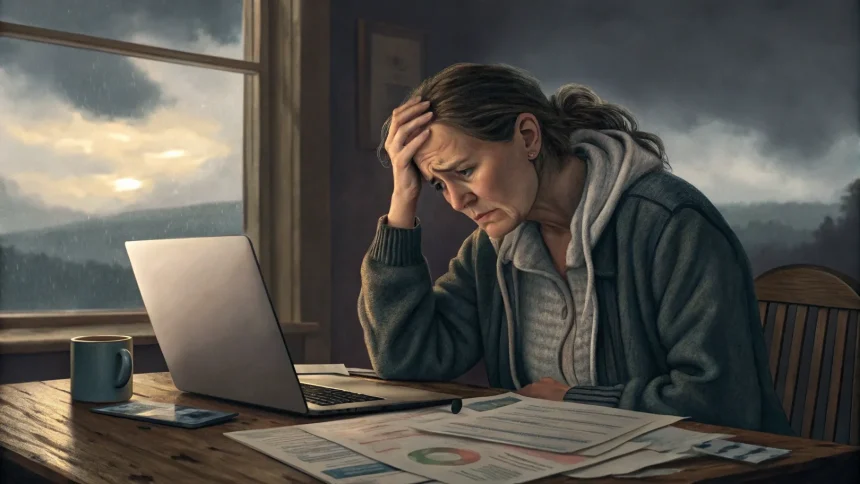

A mother’s attempt to restart her business has been denied after financial hardship following her daughter’s death led to missed loan payments. Tiffany Bramley applied for a loan to revive her business operations but was rejected by lenders who cited her payment history as the deciding factor.

The case highlights the rigid nature of lending criteria and raises questions about how financial institutions handle applicants facing extraordinary personal circumstances. Bramley’s situation represents the difficult intersection between personal tragedy and business finances that many entrepreneurs may face.

Financial Impact of Personal Loss

According to information provided, Bramley fell behind on her financial obligations during the period following her daughter’s death. The emotional toll of losing a child was compounded by financial strain, creating a situation where keeping up with payments became impossible.

Financial experts note that major life events like the death of a family member often create ripple effects through all aspects of a person’s life, including their ability to maintain business operations and meet financial commitments.

“When someone experiences a profound loss, their financial situation can quickly deteriorate as they deal with grief, funeral expenses, and potentially reduced work capacity,” explains a financial counselor familiar with similar cases.

Business Restart Challenges

Bramley’s attempt to secure new financing to restart her business operations represents a common challenge for entrepreneurs who have experienced financial setbacks. The rejection points to the challenges faced by small business owners with imperfect credit histories, regardless of the circumstances behind them.

Small business advocates point out that traditional lending models often fail to account for extraordinary circumstances:

- Credit scoring systems typically don’t distinguish between different reasons for missed payments

- Most loan applications don’t provide space to explain personal circumstances

- Few lenders have hardship policies that extend beyond temporary payment deferrals

Alternative Financing Options

For entrepreneurs in situations similar to Bramley’s, financial advisors suggest exploring alternative lending options that may take a more holistic view of an applicant’s situation.

Community development financial institutions (CDFIs), peer-to-peer lending platforms, and business grants specifically designed for entrepreneurs facing hardship may offer paths forward when traditional banks decline applications.

Some business owners in similar situations have found success with crowdfunding campaigns that allow them to share their story and receive community support while restarting their ventures.

Business mentors also recommend working with credit counseling services to develop a plan for improving credit scores and demonstrating financial recovery before approaching lenders again.

The case underscores the need for greater flexibility in lending practices, particularly for small business owners who have faced exceptional personal circumstances. As Bramley continues to seek options for restarting her business, her situation serves as a reminder of how quickly personal tragedy can impact professional aspirations and financial standing.